Economic Advisory Report: October 2023

October 27, 2023Duration: 18:32

Podcast: Play in new window | Download

This quarterly economic report, published by ITR Economics, features data specifically for the material handling industry to assist MHEDA members plan for the year ahead. The full detailed report is available to members only.

Order and Download Free Report (member login required)

Ten Key Insights from the Q4 2023 MHEDA/ITR Report “The State of the Economy Looking Forward”

-

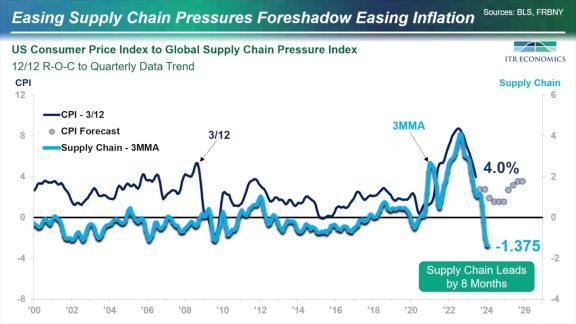

While many headlines suggest the US economy may be able to avoid a recession after all, our (ITR) analysis suggests that is not likely. While the leading indicators remain mixed, the most convincing evidence still points toward a mild recession with a late-2024 low.

-

Annual US Material Handling Equipment New Orders totaled $47.9 billion, up 10% from the same year-ago level.

-

ITR expects Material Handling Equipment New Orders to rise into early 2024. New Orders have been relatively resilient to downside economic pressures such as elevated interest rates. We are forecasting annual New Orders decline from the first half of 2024 into early 2025.

-

On the leading edge of the economy, we are seeing green shoots of recovery in single-family residential construction. The tight supply of existing homes supports an underlying need for new construction, but affordability remains a constraint largely due to elevated interest rates.

-

While it can be daunting to face a year of contraction, recovery in the housing market serves as an encouraging reminder that this decline is temporary.

-

The ongoing United Auto Workers (UAW) union strike may impact current Production, as negotiations are ongoing. If successful negotiations lead to a prompt resolution, the current outlook will remain unchanged. We are closely monitoring the situation, and we will revise our forecast if needed based on further developments.

-

Decline in Annual Production is imminent. US exports are sharply decreasing, as many of the US trade partners are also are on the back side of the business cycle.

-

Real incomes are rising, and we expect inflation to diminish further and the labor market to remain relatively strong. Together, this should put US consumers, who are the backbone of the economy, in a position to support rise for the macroeconomy in 2025.

-

Rise will resume for most industries in 2025. Opportunity can be found in countercyclical and nondiscretionary markets; those which have received federal funding, such as semiconductors and renewables; and younger industries, such as e-commerce.

-

2025 will generally be a year of moderate rise; a return to record highs will likely occur beyond the forecast range, during the second half of the decade.

Takeaways for Your Business:

-

Utilize our market forecasts for your planning and have contingency plans for both the upside and downside.

-

In addition, think back to previous economic booms – what do you wish you had done during the downturn to set your business up for success? Time those actions so you can capitalize on the general rise during 2025 and much of the second half of this decade.

-

Look for ways to lean into your competitive advantages and take the time to address any competitive disadvantages you may have. Extra time may afford an opportunity for system upgrades or efficiency improvements.

-

Lastly, we expect the labor market to remain relatively tight. Look to retain and cross-train key, high-performing employees to keep the business running, and look for ways to minimize your dependency on labor through efficiency gains.

Order and download (member login required)

Related Podcasts and Videos

Economic Advisory Report: July 2023

July 25, 2023Duration: 19:34

This quarterly economic report, published by ITR Economics, features data specifically for the material handling industry to assist MHEDA members plan for the year ahead. The full detailed report is available to members only. Order and download the new report as well as past archived issues (requires member login). Ten Key Insights from the Q3 […]

ESOPs 101: Employee Stock Ownership Plans

July 17, 2020Duration: 31:53

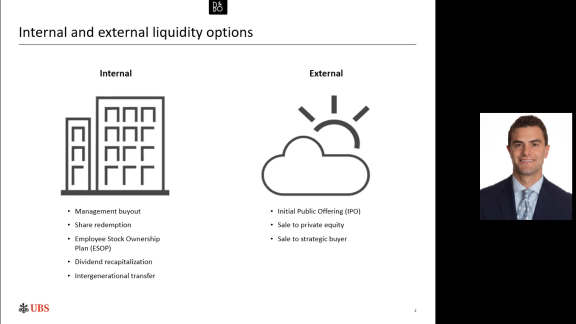

This presentation will cover the basics of ESOPs. Nick Francia, partner of The Capital ESOP Group – UBS Wealth Management and a nationally-recognized speaker on the topic of ESOPs, will start with an overview of the different internal and external options that a business owner has to sell or transition their privately-held business. From there, he […]

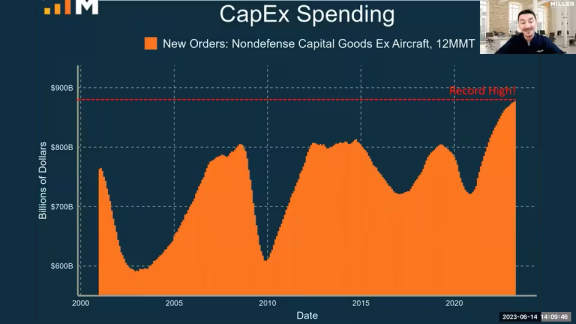

Macroeconomics: B2B Capex, Inventories, and Investment Considerations

June 15, 2023Duration: 43:15

A slowing macro economy is a headwind for investment, affecting everything from capacity planning to capital expenditures and inventory levels. The pandemic-era swings in both supply and demand are calming, but persistent uncertainties – the war in Ukraine, the Fed’s interest rate policy, and the severity and longevity of the economic downturn – all cloud […]